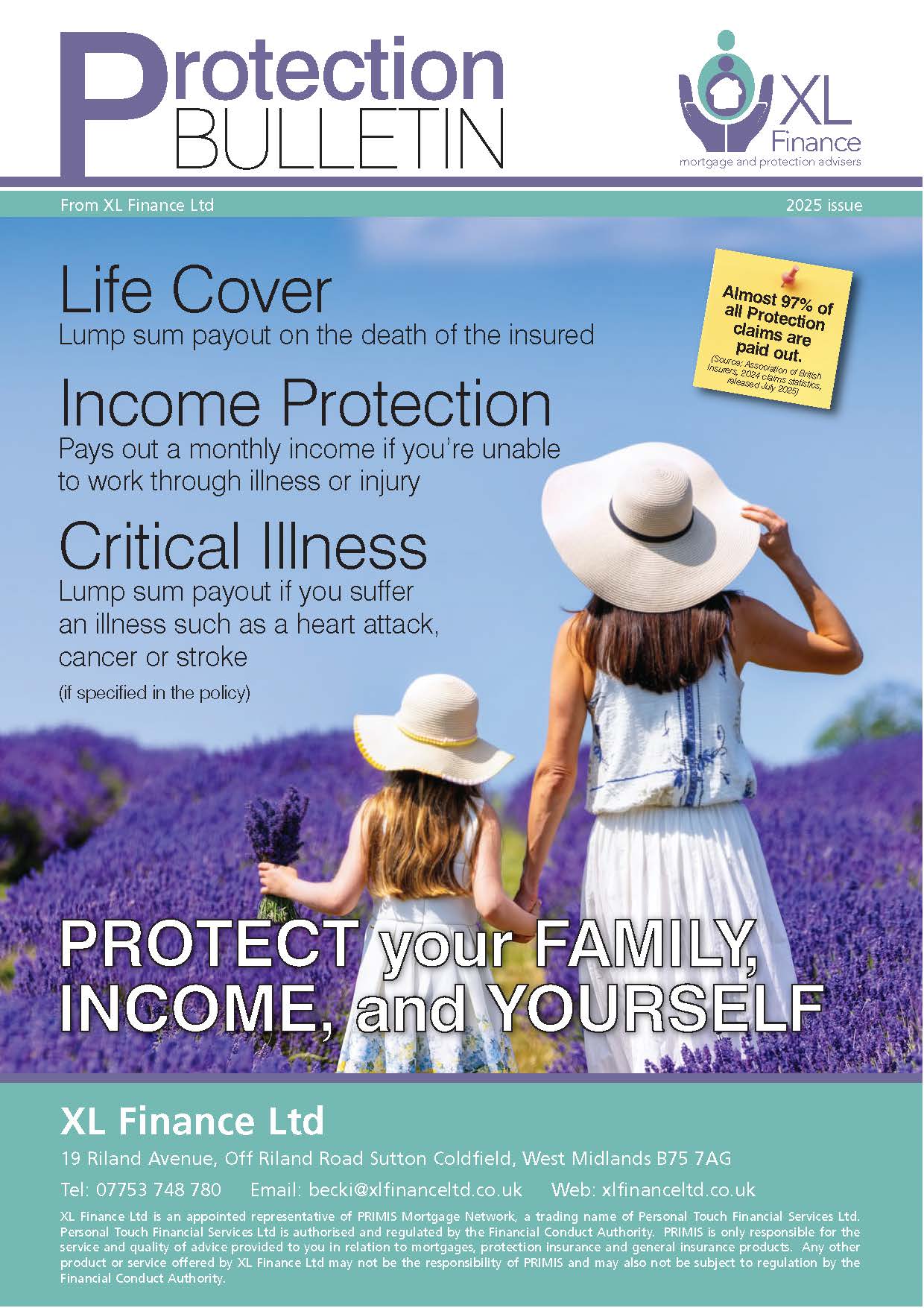

Protection

Think of your life as a Jenga Tower … you build those blocks, you work to pay out for cars, fuel, childcare, food, socialising, clothes, hobbies, debts, phones, tv subscriptions, gym subscriptions, your daily coffee – the list goes on and on!

What happens when the bottom building block is pulled away from your tower? … It wobbles precariously and could come crashing down.

Risk Calculator

check out your Risk Reality to find out what life may have in store for you.

XL Finance aren’t affiliated with LV *

Prepare for the Unexpected

The bottom Jenga block is YOU! If you die, or get cancer or suffer with a long term illness and cannot work, your income could stop. What do you think would happen when faced with the unexpected? Would you be able to rely on the State to keep you and your family afloat financially? Trust us, that won’t keep you and your family living in the way you usually do and this is why we highly recommend you obtain a suitable Protection to ensure that your payments can be met when you cannot work.

Your Needs & Budget

XL Finance Ltd doesn’t just saddle you with a massive debt (let’s not pussy foot around, calling a Mortgage a Mortgage does not detract from the fact that it is a debt – the biggest & longest debt you will ever have) we aim to settle you into your Dream Home and keep you there should the worst happen.

We consider your personal and financial circumstances carefully as a whole then offer a holistic recommendation based upon your needs and budget.

> Life Insurance

Cutting to the chase, this is Death Cover. Would you rather leave behind a debt or an asset for your loved ones? Simply put would you like for your family to stay in their home with the mortgage debt paid off, not leaving them with the uncertainly of wondering how they are going to meet the mortgage repayments or the trauma of having to sell the home? Imagine your partner is taking a career break to look after your small family, would you want them to be forced to return work full time, putting your children into costly childcare because they cant afford the mortgage, or would you rather the mortgage be paid off, with the security of an income to replace your lost earning that your family don’t have added stress at an already difficult time?

Or vice versa, imagine having to give up your job to go part-time to look after your children because you cannot afford the childcare if your partner who is part-time/ stay at home passes away.

These thoughts aren’t sexist, it’s a conversation every family / couple should be having, even if you don’t have children – would you like your partner to have to sell your home because they cannot afford to stay?

When we propose Life Insurance Cover for you, we consider not only the debts / mortgage you have outstanding, we consider the people who depend on you and how they would cope without your income.

Life Insurance can be paid as a lump sum or an income.

> Critical Illness Insurance

This is your Cancer Cover, 1 in 2 of us born after 1960 will be diagnosed with Cancer in our lifetime* – we all know someone who has suffered from this cruel disease, and everyone knows a family who have had to deal with the heartbreak alongside an uncertain financial future when a family member gets a long term illness diagnosis** The main claims for Critical Illness are Cancer, Heart Attack, Stroke, MS & Children’s conditions. There are many other conditions covered in policies including less advanced cancers, with providers offering additional severity based payouts … we understand that every condition is serious, and despite view to the contrary insurers DO want to pay out hence why they make partial payments for less severe diagnoses.

Many providers also offer additional benefits that you can use from DAY ONE of your Policy (not just at claim stage) such as a combination of any of the following:

- 247 GP Access with Prescription Services

- Physiotherapy

- Mental Health Counsellors

- Bereavement / Carer / Workplace Stress / Return to Work Support

- Dedicated Cancer Nurse

- Health MOTs

- 2nd Opinion / Best Doctors

- Gym Discounts / Nutrition Guidance / Fitness Programme

This is why it is imperative to get advice, many policies bought via comparison sites do not offer these additional benefits.

Critical Illness can paid as a lump sum or an income, you can use this to pay off your mortgage, head abroad for treatment not available in the UK, have your partner take unpaid leave to help you convalesce, modify your home, the possibilities are endless and mean that you can concentrate on getting well again.

Being financially secure will relieve you of one less stress, when life is stressful enough.

* Source1 https://www.cancerresearchuk.org/health-professional/cancer-statistics-for-the-uk

**Source 2 https://www.macmillan.org.uk/get-involved/campaigns/cancer-a-costly-diagnosis

> Income Protection Insurance

Removing the jargon, this is your own Personal Sick Pay – you may get sick pay from work if you work for a large employer or the Civil Service. For example you may receive 6 to 12 months full pay, or 6 months full reducing to half for 6 months depending on your employment contract, but many people only get Statutory Sick Pay (also known as SSP). For 2021 SSP is £96.35 per week, see here for up to date amounts https://www.gov.uk/statutory-sick-pay/what-youll-get

- Can you pay the mortgage (or rent), bills and living expenses on this per week?

- Do you have an emergency fund of 3 to 6 months outgoings?

- If you do have an emergency fund do you want to see your hard earned savings dwindle?

Legal & General* produce a yearly report called Deadline to Breadline which can be viewed here, it is worth 3 minutes of your time – https://www.youtube.com/watch?v=96E29bpT_J4

This report shows that the average household is just 24 days from the breadline, when most believe they could last for 90 days, 2 in 5 households have less than £1,000 in savings – yet for some reason do not think that Income Protection is needed? Go figure …

Most of us couldn’t cope with a sudden loss of income of us don’t and this is why we need insurance.

We arrange Income Protection to kick in when your FULL sick pay ends, meaning you can continue to live without suffering financially, the also compliments Critical Illness Insurance as this would pay out for conditions such as Mental Health and Musculoskeletal conditions.

Remember your Income bottom Jenga Block … this needs protecting.

*we are not affiliated with L&G, we look at a range of providers for your insurance needs, however this is a powerful message, and a wake up call for some.

Which Insurance is Best for me?

These insurances do different things, Life Insurance is easy, if you die it pays out. Critical Illness and Income Protection Insurance compliment each other.

Our motto is “a little bit of everything is better than nothing”, we also use the old cliché of “not putting all your eggs in one basket”, we also like to “edge your bets” … You see what we are saying here, we spread your risk approaching this holistically and realistically with a budget that suits

Imagine these scenarios:

- You get diagnosed with Cancer, need to have an operation and Chemo, you will be off work for 12 months and only get 1 month sick pay

Critical Illness AND Income Protection Insurance will pay out here

- You have a Heart Attack and are off work for 1 month, work pays 6 months of full pay if off sick

Critical Illness will pay out here, if you just took out Income Protection there would be no pay out

- You fall down at work and hurt your back, you are off for 18 months until you can have an operation to repair a disc

Critical Illness won’t pay out here but Income Protection will

All these factors need to be taken into account when looking at a Protection Package to suit you, as we said earlier, it is imperative to look at this as previously mentioned; holistically and realistically, creating a package that suits you, with a budget that suits your pocket.